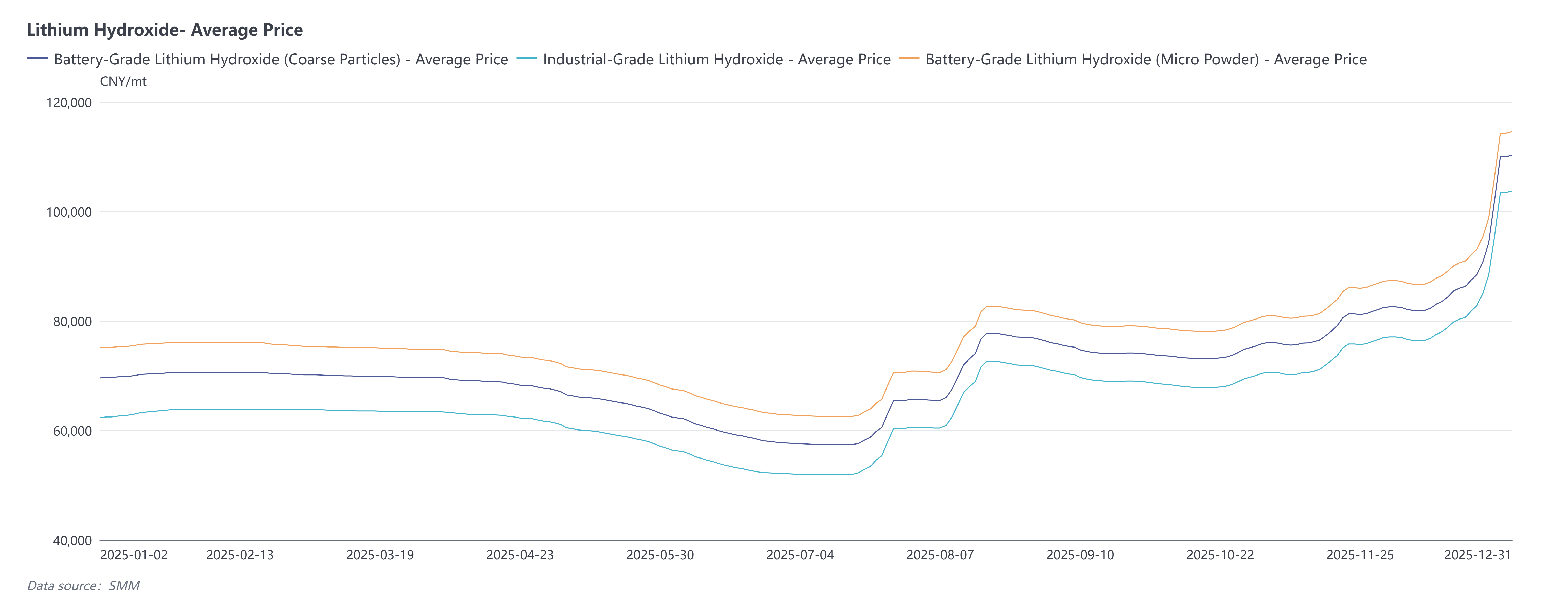

Price Review

In the first half of 2025, factors such as concentrated pre-holiday (Chinese New Year) restocking by downstream consumers, an increase in tolling volumes, and tepid spot market demand collectively led to an overall weak willingness for spot purchases in the market. Concurrently, market inventories remained relatively high, while prices for lithium ore and lithium carbonate continued to soften.

In the second half of 2025, downstream demand performed better than expected, generating additional spot demand beyond long-term contract fulfillment. At the same time, the stability of tolling supply showed signs of weakening. Driven by the recovery in lithium carbonate and lithium ore prices, market sentiment shifted towards exuberance. Downstream ternary cathode material plants began restocking ahead of schedule. Meanwhile, upstream producers, facing increased raw material costs, widely adopted a "production-to-sales" strategy, and their collective willingness to support prices strengthened. These factors combined to drive a sustained upward climb in lithium hydroxide prices.

Supply Side

In 2025, China's lithium hydroxide production reached 305,000 metric tons, representing a year-on-year decrease of 14%. The industry's annual operating rate remained below 50%. In the first half of the year, despite minor output increases from the commissioning of some new smelting capacity, overall production stayed at low levels due to weak demand growth, which prompted some smelters to proactively reduce output. On the conversion side, most enterprises operated at a loss due to lithium carbonate price volatility, leaving only a handful of traditional conversion plants in operation.

In the second half of the year, as seasonal demand picked up and lithium carbonate prices surged significantly, lithium hydroxide prices gained upward momentum. This encouraged a few smelting enterprises to switch their flexible production lines back to lithium hydroxide. Entering the fourth quarter, incremental output from the ramp-up of some new capacity led to a slight increase in smelting production compared to the first half. The price recovery also stimulated production enthusiasm among some conversion plants. Coupled with the deferred shipment of previously exported material to the fourth quarter, conversion output also experienced modest growth during this period.

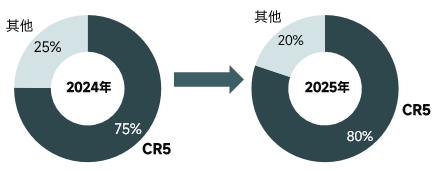

In terms of industry concentration, the CR5 (combined market share of the top five companies) in the lithium hydroxide market increased further, indicating a continued rise in market concentration.

Import and Export

In terms of exports, overseas production of ternary cathode materials has been weak since 2025 compared to 2024. Some ternary material orders shifted to the domestic market, leading lithium salt producers to redirect originally planned export orders for domestic sales. Concurrently, as overseas smelting capacity gradually came online and product quality stabilized, lithium hydroxide export volume in 2025 decreased by over 50% year-on-year, marking a significant reduction.

Regarding imports, import volume in 2025 increased by approximately 70% compared to 2024. The primary reason was order adjustments within the overseas lithium salt supply chain throughout the year, leading to shipments to China for inventory management purposes.

Demand Side

Battery Segment: In 2025, China's power battery installed capacity grew by over 40% year-on-year, with lithium iron phosphate (LFP) cells contributing the vast majority of this increase. The ternary system remained in a phase of structural adjustment. Approaching year-end, automakers released production plans earlier than usual, coupled with the imminent closure of vehicle purchase subsidy windows in many regions, which boosted activity in the vehicle market. This, in turn, drove overall improvement in demand for battery installations.

Material Segment: Throughout the year, domestic demand for ternary cathode materials followed a trajectory of "gradual increase from the beginning to the end of the year." Specifically: In Q1, the market was generally subdued due to the traditional off-season. In Q2, demand began to recover, driven by rising raw material prices. In Q3, the market improved further, aided by the traditional stocking season ("Golden September, Silver October"). In Q4, demand reached its annual peak, influenced by expectations that some subsidies might be phased out the following year, combined with rising raw material prices, leading to front-loaded order releases. Entering December, demand is expected to retreat as the peak season concludes. Against the backdrop of significant raw material price volatility throughout the year, ternary cathode manufacturers widely adopted a "production-to-sales" strategy, generally avoiding building additional inventory.

Market Balance and Inventory

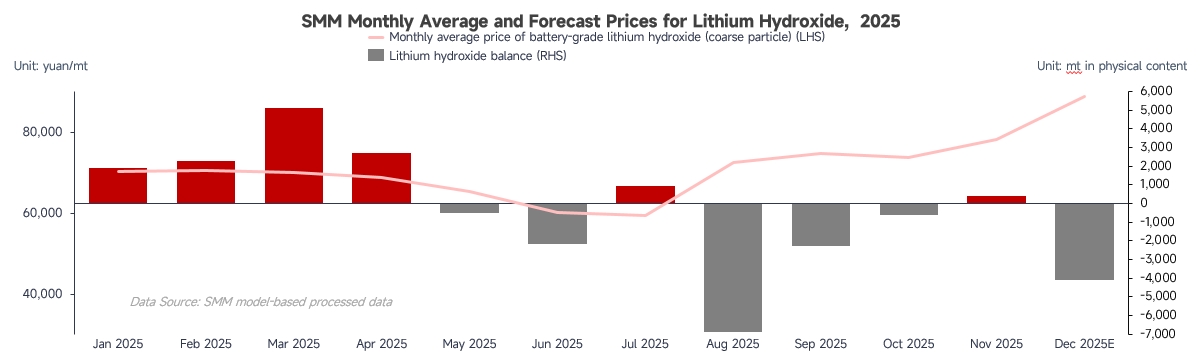

In 2025, the lithium hydroxide market experienced slight inventory accumulation in the first half of the year but achieved effective destocking in the second half. The overall supply and demand for the year showed a slight tightness. Driven by the hedging profits from lithium carbonate futures, upstream producers not only flexibly adjusted output based on price and order situations, strictly adhering to a production-to-sales strategy, but some traders also utilized futures-spot arbitrage and lithium carbonate-lithium hydroxide price spreads to conduct operations. This absorbed part of the market's accumulated inventory, leading to a contraction in circulating supply, especially since year-end.

Regarding inventory, the lithium hydroxide market in 2025 generally exhibited a pattern of "reduced supply and increased demand," remaining in a destocking trend throughout the year. In the first half, due to slow demand growth from downstream ternary cathode materials and a significant reduction in exports, the market accumulated inventory overall, with days of inventory remaining high. In the second half, during the third quarter, renewed downstream demand spurred stockpiling behavior, leading to a continuous decline in days of inventory at lithium salt producers. By the mid-to-late fourth quarter, as prices remained high and demand growth slowed, downstream players focused on consuming existing inventory and fulfilling long-term contracts, conducting only minor purchases for rigid demand. This further reduced days of inventory. Overall, the market's days of inventory in 2025 showed significant improvement compared to 2024, with the industry operating at a more rational, sales-driven pace.

2026 Outlook

Supply Side: Lithium hydroxide supply will continue to be dominated by the smelting sector. Most leading lithium salt producers possess flexible production lines or lithium carbonate conversion capabilities. Coupled with the incentive from hedging profit potential, they are expected to continue implementing the production-to-sales strategy. Expansion plans by a few leading smelters in recent years will bring some incremental supply in the future. On the conversion side, due to high lithium carbonate prices, the number of operating traditional conversion plants is limited, with only a few enterprises possessing salt lake raw material resources able to maintain profitability. Therefore, only marginal growth is expected from the conversion sector. With the advancement of expansions by leading smelters, domestic lithium hydroxide production is projected to grow by approximately 16% in 2026.

Demand Side: The pressure from lithium iron phosphate (LFP) on the ternary cathode material market is expected to persist. Combined with a slowdown in the sales growth of terminal new energy vehicles, the upside potential for the ternary market may be relatively limited, with its subsequent growth rate expected to gradually narrow. However, long-range capability remains a long-term development direction for new energy vehicles. Ternary materials, leveraging their high energy density advantage, will continue to hold an important position in the market. Furthermore, the development of high-voltage materials, demand growth from emerging sectors like the low-altitude economy, robotics, and drones, as well as the initial pull from semi-solid-state battery technology development on high-nickel ternary materials, are all expected to contribute incremental demand to the future ternary market.